Its is important each of us who are fortunate enough to have food on our table make sure others have food on theirs. Can I ask your support in feeding the homeless and those in need this Thanksgiving?

Consider giving a buck or two and I will match a portion of the funds to the food bank of your choice.

Here are some photos of what we are doing at the Food Bank of Nevada County

Food bank staff and board of directors (Some of us anyway)

From our garden we provide fresh homegrown vegetables- These we grew ourselves!

We serve in incredible 12,000 HEALTHY snacks a week to Nevada County Schools beside feeding thousands a month.

The letters we get from kids are both heartbreaking and uplifting. Can you spare a few bucks to help me help the poor?

Help me help our community.

TURKEY MATTERS IS IN FULL SWING

Can I count on you? Can our hungry count on you? Let’s do it!

Its time again for our Turkey Matters food drive for the food banks of our counties.

Help me feed the poor with our annual turkey drive where we buy turkeys for the poor. I do this every year and now ask for community support. The program is easy. Just make a check out to the food bank of your choice. Do not make the check out to KVMR or me. Make it out to the food bank of your choice.

Mail: KVMR FM 120 Bridge Street, Nevada City, Ca 95959. Attention Turkey Matters.

I will match a portion of the funds with my own money to that food bank and KVMR will forward my check and yours to that food bank. That’s all there is too it! Please consider helping.

----------------------------------------

Money Matters airs this Thursday November 3, 2016 at NOON PST

------------------------------------------------------------------

Marc's Notes:

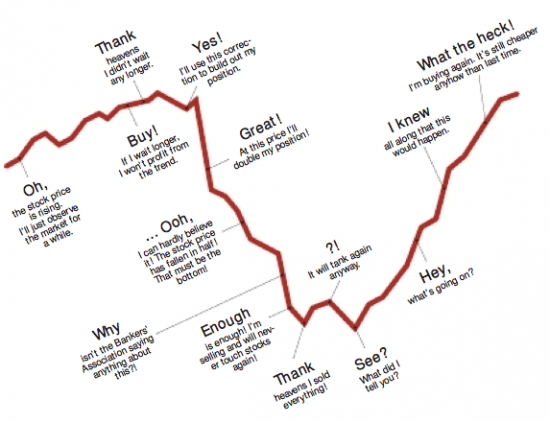

With pre- election fireworks not failing to disappoint, as is usual during elections periods, the markets apparently don’t know which way to turn. Having been market neutral to market negative in our portfolios, meaning our stance is one in line with a market going nowhere to perhaps even going down, and being that way for more than three months now, we, like the rest of the world, are wondering where the markets may go once the new president is sworn in.

With a Hillary win now looking more likely since the Donald was caught talking locker room to an extent that may have shocked even the staunchest of supporters, prognosticators are forecasting a Hillary shoe in. Of course, the election, like the market, loves fooling most of the people most of the time and calling elections, like calling markets is a fools game even for me. One can only guess once again as to what president will cause the markets to either rise or fall after all the handles are pulled.

With big banks covering both sides of the aisle like they always do by donating to both candidates, the majority of analysts agree a Hillary win means the same ol’ same ol’ for Wall Street. That being the case, a Hillary win would, if the prognosticators are correct, and they often are not, the markets should move higher.

With the wild card being the Donald and no one knowing exactly just what it is he would do, the general impression is if the Don is elected, Wall Street might run for cover due to the uncertainty. Although Donald is definitely a one percenter and understands corporate America a hundred times better then Hillary, we still don’t know how predictable this unpredictable man will be if sworn in.

Don’t bet on any of this however as markets rarely do what the majority expect them to. The markets could react in an exact opposite direction then expected when one of these folks take to the oval office, and no matter which way it goes, neither direction will surprise at least this analyst.

I have learned a long time ago: no one knows anything for certain about the market. She is a fickle beast, looking to tear you a new you know what at any time. The market can break the smartest investor or make the dumbest lucky son of a b**** an overnight millionaire. The trick to riding it however, is too strap yourself on tight, hold on and prepare to be thrown off at any time. You can accomplish this by not committing too much money in any one direction, in any one industry or on any one outcome.

We will know what the markets think of our new president in due time, and it likely won’t exactly pan out like anyone expects. That’s the thing about markets: They are impossible to predict.

--------------------------------------

With the holidays approaching, thoughts turn to family and friends. For me thoughts also turn to calories as in the consumption of them. I try and limit my intake as I am an old man now but still have young kids. I started late and so am trying to stay alive to see them go to college, marry and give me some grandkids. (Ouch that sounds bad).

Anyway, at the young age of 60, I try and work out once a day, limit my bad food intake and take things into my body to hopefully make my mind stay sharp. I read a lot about investing on all things money but also read about investing in my vessel that houses my brain which is of course by body. Many an old person has told me the brain may stay sharp but the body gives out. For that reason, I am trying to stay ahead of the game.

Besides the obvious benefits from working out with aerobic movement (circulatory benefits) and weight bearing exercises (skeletal benefits and body shape improvement) I also take a variety of supplements and foods that may (or may not) allow me to live a fuller life and keep moving through the duration of it.

People always say to envision and set goals in one’s life yet I have found no one that has set an AGE GOAL. If setting goals and visualizing things is generally agreed upon as to actually improve one’s odds at achieving those goals, I ask: why NOT set an age goal?

Just because no one does it and no one can really determine exactly what day one will meet his maker, I figure if none of the unexpected early life terminators (accident, cancer or other) puts me down prior to my succumbing of old age, why not set an age goal just for the hell of it?

Like I said, if setting goals and envisioning things is actually generally accepted as good practice, why not set an age goal right?

So a few years back I set a goal of living to be 128. Yes, that’s a bit long and would set a verifiable old age record if I actually make it, I aim to shoot high and why not.

Like a business negotiation where one always starts high on price and negotiates downward (seller of goods) or the buyer who starts LOW and works UP, I figured 128 was a good starting point. Go big or go home right?

My 91 year old tells me once I get to 90 or so I won’t want to live any longer due to the pain I will experience just moving around but I still notice he doesn’t jump off a bridge to end his life. He still wants to live.

And yes I do notice some old people who can’t walk, can’t sit comfortably, are grossly overweight or have other infirmities, afflictions that may very well affect me in due time but I don’t give up easily in anything and just because most people tell me these things are a certainty, like many things I am told in my life, I say hogwash.

Don’t tell me I can’t do something because if I think I can and I want to do it, I will tell you to go jump in the proverbial lake.

To attain a goal, one first has to believe it is attainable. Call me crazy (and many have over my life) but I firmly believe I can make it to 128. I am not saying the odds are in my favor of course, in fact the odds are grossly stacked against me, but like playing an opponent on a hot field on a hot day, my response is yes it may be hot, but it’s hot on BOTH sides of the court. The harder it gets, the more determined I get.

In other words, as was said in the movie Star Wars “Never tell me the odds”.

In the same series, it was also said by Luke in the second Star Wars movie “I don’t believe it” of which the response from Yoda was “that is why you fail”.

I am pretty much convinced you won’t live to 128, nor 118, 110 or even 100 if you don’t believe you will. If you make up your mind to fail in anything, you most likely will.

So I try not to go into anything thinking I will fail. I MAY fail (everyone does every so often) but I don’t start out with that belief nor do I catch myself believing I will fail anytime during the process.

Positive thinking wont insure you will succeed of course, and just being positive won’t make a bad plan succeed. But a good plan needs the best opportunity to succeed and that starts with doing your homework, then be willing to do the work all the while believing you will succeed.

So to get to 128 I read a lot about health. I mean a lot! I eat stuff that tastes like crap and although I don’t like things that taste like crap, I eat them (ever try Noni Juice?)

In the morning (every morning except when traveling) I take blueberry juice (rats live a lot longer fed blueberries so I read), Noni juice (this stuff is GOD AWFUL), grapefruit juice with nutritional yeast (also tastes like crap but not as bad as Noni juice), two tablespoons of raw olive oil (see the movie Lorenzo’s oil), prune juice (has tons of iron and is good for digestion), green tea (three or more cups a week helps prevent various cancers),ephedra tea (opens up lungs and stimulates circulation) and then a small bit of protein in the form of a lean meat or egg.

After that I take about 30 supplements (yes I might be wasting my money but who really knows right?).

Throughout the day I love turkey with homegrown lettuce, protein shakes ( I work out a lot so I need lots of protein), more juice, and all sorts of healthy stuff. I stay away from burgers and fries, shakes and packaged stuff but don’t get me wrong. I can polish off a box of Sees’ candy, smoke a cigarette on occasion, quaff down two or three martinis or wines and eat salami and pie with the best of them. I LOVE ice cream and other sinful foods and will eat them if I feel like it.

I don’t believe in denying myself the finer things in life because if I do why the heck would I want to live to 128 right?

The point is I have vices and bad habits but it’s not what you do once in a while that makes or breaks you, it’s what you do on a daily basis that counts. What I do daily may not be the best in the entire planet of health food nuts but what I do works for me.

Who knows, tomorrow I may get cancer, die in a car wreck or have a stroke and it that happens so be it. At least I tried. But right now I am in the best shape of my life (barring my young twenties of course). My hair is thinner and my knees and back are always sore but my body weight and shape I see in the mirror pleases me to no end.

I am still fairly sharp and can argue (or debate) with the best of them. I work hard and can multi task no problem. I try and control my temper, relax and meditate, work out and do the best I can for my clients and customers by studying constantly, always asking what if and why and always question my decisions one last time to cover the possibility “what if I’m wrong here”.

I may not make it to 128 but don’t tell me that and don’t let anyone tell YOU that something can’t be done if you know it can be. Just don’t forget to do your homework then be willing to do the work. Then believe it CAN be done during the whole process.

Do all those three things and that will give you the best chance at actually doing whatever it is you want to do and I’ll see you in year 2083 (maybe).

Jambo!

Marc