Money Matters returns to the air for the start of our summer season. Hear all about what to expect in the markets. May 17th, noon PST on KVMR and all related stations and at Moneymanagementradio.com

---------------------------------------------------------------------------------------------------------------

Reaching out......

The United Way partners with Interfaith Food Ministries (IFM) with help from the Food Bank of Nevada County with "Food Access Saturday" , a program of food distribution for those that work during the weekdays but still need assistance in feeding their families. Food is available the second Saturday of each month at IFM, 440 Henderson Street, Grass Valley, behind the Prosperity Lanes/ Beam Center parking lot. United Way (530) 274-8111. IFM (530) 273-8132.

Pictured here is Sue Vanson, Director of IFM, Paula and Jacob Senn, the first customers of the program and Megan Timpany, Director of the United Way, Nevada County.

Photo by Marc Cuniberti

----------------------------------------------------------

Hi you rabid money fans,

Wow, some markets huh? So as we enter into summer, which can be typically anemic for markets as traders head out to their vacations, the Dow seems stuck in 20,000's and may be trying to assault 21,000. No one knows which way markets will go of course, Fixed income recovered some and that was mentioned in previous article I did as a possibility. I have attached that below as well as my new comments covering this recovery. I have also finished up on my weird article called "Spinners, Earthmovers, Doer’s, Dawdlers, Talkers, Slugs, Fakers, Weasels and Crooks". Previous postings of this article were done in parts so the entire article is finally here. This is tongue in cheek so please take it with a grain of proverbial salt. So that is about it for now but feel free to contact me for a no-cost, no-obligation in person consult and analysis of your financial situation. (Minimum investment portfolio > $100,00.00).

----------------------------------

Fixed Income sells off. (Published March 8, 2017)

Approved 187912

Mom and Pop conservative investors may have received a nasty pre-Christmas present in the form of lower portfolio balances. Although premarket indicators of market direction looked horrific on election night, the day the market opened on November 9th the market took off and has barely missed an upbeat. The most commonly watched indicator, the Dow Jones Industrial Average (DOW) climbed steadily over 19,000 for the first time ever and closed out the month there. This month end close is a significant indicator to some technical analysts and indeed an obvious indicator to many that the Trump rally at least for now is for real.

Not all stocks rose in value however as is the case with market rallies and a handful of sectors reacted in the opposite direction and some sectors fell with relatively shocking speed and percentage. Technology sold off hard while defense and infrastructure soared.

Where the conservative investor got hammered is in the fixed income markets. Fixed income refers to things like corporate bonds, treasuries, municipal bonds, utilities, preferred stocks and just about anything else that pays a fixed interest rate or perceived as doing so.

This area of investment is generally thought of as more stable way to play the markets due to their fixed promise to pay out income in the form of dividends or interest and many conservative investors have been told these types of investment are less volatile than traditional stock holdings. As such, older investors or those with less risk tolerance usually hold a large percentage of fixed income in their portfolios.

Fast forward to the Trump rally and a wakeup call of sorts as to how markets can operate shocked many an investor. With a sudden spike in interest rates on November which continued during the following weeks, fixed income assets basically got creamed.

From CBC News: Bank of Montreal economist Benjamin Reitzes said Monday: "The price on 30-year Treasury bonds fell nearly five per cent on Wednesday, erasing two full years of coupon payments." The article released November 14th went on to say: "The bond market is supposed to be a dull, boring, stable place," said Colin Lundgren, head of U.S. fixed income at Columbia Threadneedle Investments. "Instead, it's been at the centre of the storm."

An understatement to say the least. Across the board fixed income continued to bleed red in an uncharacteristic freefall that likely put a big dent in conservative portfolios likely causing many a phone call to advisors everywhere asking by their clients to explain just what the hell happened to holdings thought to be somewhat immune to such sell offs.

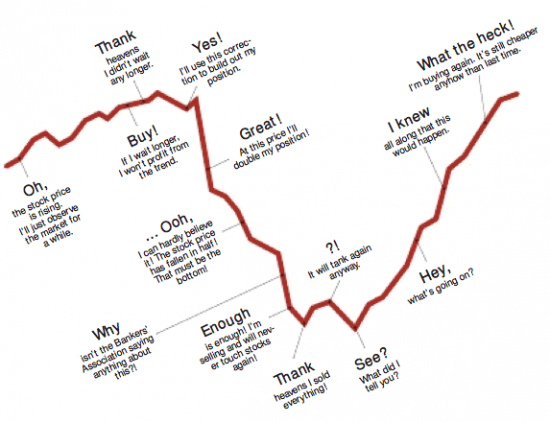

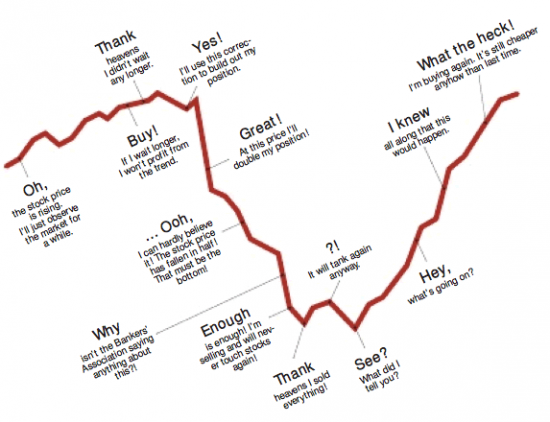

Luckily for fixed income investors, the nature of how fixed income works may be self-correcting. As the price of a fixed income security drops, their yields rise, so investors buying at destressed prices will get higher yields as prices continue to fall. This type of slingshot of rates versus prices can entice new buyers into a falling market and at some point yields get too juicy for new investors to resist. This is not to say prices can’t keep falling. They can.

No one knows just when prices on fixed income might stabilize but for now the steep plunge witnessed seems to have at least slowed for now. But the damage has been done. Apparently the market perceived a Trump presidency as one which will let rates rise, a comment Trump himself indicated when he said during the first presidential debates “because of record low interest rates from the Fed, the country's economy is in a big, fat, ugly bubble…..”

One might draw the conclusion and the market apparently did, that Trump believes low rates are a scourge to the economy that should be corrected, which means allowing rates to rise. When rates rise, fixed income goes in the opposite direction, and for now that direction is causing angst for many an investor.

As in most drastic markets movements however, selling into a panic is a practice that should be carefully analyzed before undertaking. Sometimes the market overreacts and throws babies out with the proverbial bath water. Patience may be the order of the day.

-------------------------------------

Fixed Income Recovers

198335 approved

After Trumps November 8th election win, no one really knew how the markets would react the day after on November 9th. Stock futures, which give an indication of what overnight traders are doing first showed a horrendous correction was coming when the market opened and gold skyrocketing higher. Not so when the opening bell rang next morning. Stocks took off and gold fell. What really shocked investors and not in a good way was the selloff in fixed income. This area includes bonds, preferred stocks, treasuries, municipal bonds, utilities, and other investments that pay a fixed rate of return and are regarded as less volatile than traditional stocks. This type of investment is likely what your grandfather held and it’s a favorite among widows, orphans and conservative investors. Normally not regarded as moving very much up or down in price, the weeks following Trumps victory witnessed a virtual blood bath in fixed income.

"The bond market is supposed to be a dull, boring, stable place," said Colin Lundgren, head of U.S. fixed income at Columbia Threadneedle Investments. "Instead, it's been at the center of the storm."

As I wrote in December article entitled “The fixed income sell off”, fixed income does have a self-correcting type of quality to it which at that time might have calmed the nerves of those conservative investors who saw balances drop in speed out of the ordinary of what they were used to seeing.

When prices drop on the price of a fixed income investment, because the interest it pays is fixed, the yield to new investors buying in after the drop goes up. That means investors buying at destressed prices will get higher yields as prices continue to fall. This type of slingshot of rates versus prices can entice new buyers into a falling market because at some point yields get too juicy for new investors to resist. One might also add when investors panic, they sometime throw the baby out with the bathwater and what would otherwise be a modest sell off suddenly becomes an all-out rout. This can cause the price pendulum to swing in one direction (down) to the advantage of those willing to step in with cash to scoop up some perceived deals which in the fixed income market means better yields.

Apparently at least some investors took the bait and starting a few months after the sell-off prices began to climb in many fixed income markets and continued to do in the recent weeks. Not to say the sell-off couldn’t begin again as no one can predict market directions but sometimes common sense, knowing how certain investments perform and some basic math can lead to some good buys in the markets.

-----------------------------------------

Spinners, Earthmovers, Doer's, Dawdlers, Talkers, Slugs, Fakers, Weasels and Crooks

What does it all mean? Fancy words or animal decryptions?

Actually these are my own classifications of different types of people as they relate to their own career path.

Sounds confusing but read on and see if you recognize any of the work types described below.

The easiest to spot are the Earthmovers and Crooks. Earthmovers start those incredible companies that revolutionize how we live in some way or another. They may or may not be college educated, and many attend Ivy League schools only to drop out midway through because they know their ideas don’t need degrees to make them work. Bill Gates, Mark Zuckerberg, Steve Jobs and Elon Musk come to mind. Billionaires all of them and they have changed the way we live our lives through their genius. As for community, Earthmovers usually operate alone or in pairs.

Crooks are also easy to understand and identify. They are basically, well, crooks. They lie cheat and steal to make a living and are usually a victim of a personality disorder or two. Crooks operate alone but if you find two of them in cahoots, the con is usually much bigger in scope.

Easy enough but now let’s look at the others.

Doer’s are good folks. They are the pragmatic ones. They start small businesses that usually succeed. They also make good employees and know the value of a buck. They work hard and treat others fairly. They are usually honest and live fruitful lives that contribute to society and they rarely take handouts unless badly needed and then only do so temporarily. Most of the working class fit in here and likely you do to. Doer’s operate solo or in groups of any size.

You can recognize Dawdlers, Talkers and Slugs because they have many similar characteristics.

Dawdlers just don’t want to work and think the world is one big jelly bean field where they can lie around and write poetry. None of this “conformist working nonsense” for them. Dawdlers idle away their hours in coffee houses, hiking or hanging out at the river during the day while everyone else is working.

Talkers, like Dawdlers also don’t like working much but spew forth verbal diatribes to counter their low self-esteem which got that way by not working. Talkers might make up many of the people you see during a daytime protest rally. They’re there because they’re not working. Talkers often end up as activists or working a few hours a week at a non-profit to convince themselves their unemployment is necessary so the world can hear their point of view. Like Dawdlers, they are often on the public dole while complaining about the very system that gives them their checks. Dawdlers and Talkers can’t make it in the private sector where performance is actually expected so they operate around the fringes of normal society. Both Dawdlers and Talkers are usually found in large groups.

Slugs have similar characteristics as Dawdlers but Slugs just can’t catch a break. They rarely hold jobs longer than a few months and constantly blame others or circumstances out of their control for their plight. When you catch up with a slug, which is easy to do, they will always tell you how hard their life is and how bad luck follows them like the plague which is usually true. Although the world is full of Dawdlers and Talkers, you won’t run into many Slugs. Their lot in life is so sorrowful apparently God didn’t make many of them and that’s a good thing. Slugs live solo except for the rare occasion where a mate is found that takes care of them.

Fakers are like Talkers as both usually have outward personalities. Fakers attempt to appear like Doer’s but much of it is illusion and therein lies the difference. Fakers usually have long resumes with many jobs listed and their spotty work resume shows a nomadic quality to it. They move jobs and locations often and may attach self-made titles after their names. A variety of letter designations you likely have never heard of trail their signature page. These people may end up end becoming the proverbial life coach or a consultant of some kind. They also can move in and out of careers where a few months of study can yield an impressive sounding certification like realtor or physical trainer. No offense meant to you hard working folks in these careers of course. It’s just that Fakers are the type that enter your field then leave when the going gets tough and muck up the business for the rest of you. Heaven help the people who follow the advice of such characters. They are where they are because they can’t hold a real job for any length of time. Fakers usually operate alone but support each other to further each other’s illusion.

Weasels are similar to crooks but don’t actually break any laws, at least most of the time. Weasels are a sort of con artist but use legal techniques to borrow or garner money from others and then just don’t pay it back. The excuse is the investment or whatever didn’t work out and your money is then gone. The living expenses of the weasel was usually taken from such “investment” money. This is how the Weasel survives. Like monetary locusts, they move from sucker to sucker all the while telling a good story. Many Weasels are not real crooks but just delusional to the point of believing their own schemes. Even with a history of failed endeavors the delusional mind of the Weasel never makes the connection. Weasels occasionally find themselves in lawsuits revolving around one or more of their failed endeavors. As for community, Weasels almost always operate alone.

Last but not least come the Spinners. Spinners come from a wide variety of backgrounds and they are a common bunch. They may hold good day jobs as a main source of income or they may spend their life on the eternal treadmill of their spinning.

Spinners are like cars stuck in the mud. The wheels turn but they don’t go anywhere. If they do, they usually don’t go far. Spinners have grandiose ideas and go whole heartily into each endeavor. The problem is Spinners aren’t pragmatic, usually don’t possess the common sense or diligence of the Doer’ and don’t have the fortitude to make their projects stick for any length of time.

Spinners usually start business after business or website after website. If working real jobs, they often use their salaries to finance their “ideas” which rarely go anywhere, which is why most Spinners will never get rich. Spinners tire easily of the nitty gritty work necessary to make a real go of things and eventually get bored and then move on to next project or idea. One month they’re selling vitamins, the next month opening up a restaurant. They usually have many failed websites and businesses to their name because each one eventually peters out in lieu of the next new idea.

If the spinner doesn’t hold a day job, he or she is usually broke or worse yet, in heavy debt.

Spinners are vast in number and are one of the reasons new businesses have such a high failure rate. Spinners are also responsible for many a failed marriage or friendship as funds are usually needed to start each endeavor and the money disappears down the rat hole of the Spinner’s latest failure. Spinners can operate alone or in groups but a group of Spinners usually results in enough blame to go around for everyone as the inevitable happens. In a comedic twist, two fakers operating together can be mistaken for a pair of Spinners.

In conclusion, there are many variations of each classification and sometimes people can possess multiple qualities of each in differing degrees. Also keep in mind these are my own classifications. I am not a psychologist or an expert in human behavior. It’s just my attempt at explaining common traits that I have witnessed over the course of 45 years of being in the business world.

What’s your experience? Do any of these traits seem familiar? How about your reaction to this article?

Just so you know, Earthmovers won’t ever read this being too busy but the Doer’s will love it. Dawdlers, Fakers and Talkers will hate it with a passion as it flat out nails them and they will likely lash out at me. Spinners will wonder if we are talking about them and Weasels are too delusional to make the connection. Slugs won’t get it which is their ongoing problem on everything and Crooks just won’t give a damn. So now you know who you are!

--------------------------------

Your financial advisor hard at work on another type of "work". Do you recognize the musician I am playing with?

He does live here locally! It was a great experience for me (and hopefully) him as well. He stumped me at times but HE had a hard time keeping up at others.

All for now and Jambo!

Marc