Can I Make More Money If I Roll Over My 401(k) Into An Annuity?

YES NATIONWIDE INCOME WITH BONUS CAN PAY NORTH OF 10% A YEAR

CONTACT ME FOR YOUR PAYOUT PERCENTAGES- THEY MAY BE HIGHER THAN YOU THINK! (530) 559-1214

28

Ashley Kilroy

Sat, June 10, 2023 at 6:00 AM PDT

When you leave a job where you had a 401(k) it’s important to understand what your options are for rolling over your tax-advantaged plan. Cashing out is another option but can result in significant taxes. Many choose to roll their money into a new 401(k) or an IRA, but an annuity is also a viable option. Here’s why an annuity may be ideal for your 401(k) rollover and how to conduct the process.

For more help with a 401(k) rollover, consider working with a financial advisor.

401(k) Rollover Definition

A 401(k) rollover is when you transfer the money from a 401(k) to another retirement savings account. Doing so allows you to simplify your retirement savings plan in different situations. For example, if you find a new job or retire, you can bring your old 401(k) with you and deposit your money into your new employer’s plan.

On the other hand, you might leave a job for another that doesn’t offer a 401(k). In this case, you might roll over your funds into an individual retirement account (IRA) or an annuity. Similarly, if you find a retirement savings vehicle with better returns than your 401(k), a rollover is also an option.

There are two ways to roll over your 401(k): direct and indirect. With a direct rollover, you provide your new retirement account information to the manager of your current plan. Then, the manager sends the funds to your new account.

Conversely, an indirect rollover means liquidating your account. You’ll receive a check in the mail and must deposit the funds into a new account within 60 days or pay income taxes plus a 10% early withdrawal penalty if you’re under age 59.5 (or 55 if you’re retired). That said you can pocket a portion of the cash and pay the taxes due or keep some of the money if you’re strapped.

How to Roll Your 401(k) Into an Annuity

Putting your 401(k) money into an annuity is another option. An annuity is a contract guaranteeing payments for a specified period of time. Insurance companies accept 401(k) rollovers to fund annuities. Here’s how to handle it:

Make a Plan

It’s recommended to discuss your rollover ideas with a professional. A financial advisor will help you find the best annuity for your unique situation. In addition, they can oversee the rollover to ensure everything is correct.

Choose an Annuity

As with any financial decision, it’s best to shop around. Talk to multiple annuity companies and get the details on each offer. Then, you can compare each plan’s structure and fees. In addition, you can check how financially stable each company is and choose one that gives you confidence.

Communicate with Your Chosen Company

Once you make your pick, communicate with the annuity company. Let them know you want to purchase a contract and roll over funds from another retirement plan. Your financial advisor can also facilitate this communication.

Send Instructions to Your Plan Administrator

Once you’ve acquired the annuity and filled out the necessary paperwork, instruct your 401(k) administrator to execute the rollover. A direct transfer is the easiest way to complete the process.

How Long Does It Take To Roll Over a 401(K)?

401(k) rollovers take varying amounts of time, depending on your situation. Because the process involves multiple parties (namely, you, your old plan administrator, and your new plan administrator), it usually takes several weeks to finish.

In addition, your 401(k) type can impede the rollover. Specifically, traditional 401(k)s often take two to three weeks to roll over, while Roth accounts take longer because they have unique requirements and tax implications.

Remember, you’ll face penalties and taxes if you don’t roll over your funds within 60 days. Therefore, it’s best to stay on top of the process by frequently communicating with all relevant parties and creating a detailed plan before initiating the rollover.

Reasons to Roll Your 401(k) Into an Annuity

401k rollover to annuity

Although you can roll your 401(k) into numerous account types, an annuity offers specific advantages, including:

Reliable Income

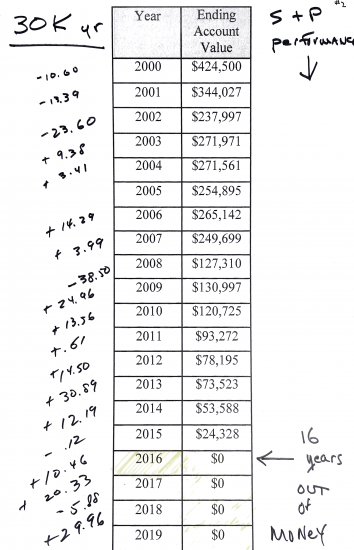

An annuity provides steady income regardless of economic changes and stock market performance. For example, a $1 million annuity can provide about $70,000 of annual income until you pass away. On the other hand, $1 million in a 401(k) or IRA will last as long as the account produces investment income and your withdrawals don’t drain the fund.

For instance, say you expect $70,000 of annual income from your retirement plan, but stock market volatility causes your portfolio to dip by 20%. Your $1 million nest egg would shrink to $800,000 overnight, and you would withdraw an additional $70,000 for that year’s expenses, leaving you with $730,000 in your account. If the economy continues struggling, you might drain your account within several years, leaving you without an income stream. An annuity avoids this possibility because your income doesn’t depend on the stock market – it comes from the company holding your policy.

Sidestep Longevity Complications

Likewise, a 401(k) can run out of funds if you live long enough. For instance, you might plan to live for 30 years after retiring at 62. However, if you’re going strong at 90, there’s a solid chance your retirement account can’t keep up with the cost of living. In this scenario, you could run out of money even if you maintain the same lifestyle for longer than you intended your account to last. With an annuity, you’ll continue receiving payments year after year, no matter how long you live.

Longer Deferral Option

Current legislation mandates that you take required minimum distributions (RMDs) from 401(k)s, 403(b)s, and IRAs by age 72 (or 73 if you turn 72 in 2023). Otherwise, you’ll owe a 50% excise tax on uncollected distributions. Roth accounts are exempt from this rule because the government has already taken taxes out of your distributions.

Fortunately, you can delay RMDs until 85 with annuities. For example, say you have a Roth IRA with $500,000, a $1 million annuity, and Social Security income. You receive $5,000 monthly between your Roth IRA and Social Security checks and currently don’t need your annuity income. In addition, adding more than a few hundred dollars to your current income will raise your Medicare annual premium by thousands. Therefore, you can delay or reduce your annuity withdrawals to minimize your tax burden and avoid unwanted financial implications.

Tailor Your Plan

Traditional retirement plans usually have cut-and-dried structures. However, annuities offer modifications (known as riders) to suit your situation. For example, you can preempt inflation with an inflation adjustment rider that raises your income by a small percentage each year.

401(k) Rollover Rules

Here are essential rules to keep in mind as you manage your rollover:

- You have 60 days to deposit the money into a new retirement account if you conduct an indirect rollover. Otherwise, you’ll incur steep financial penalties.

- If you roll a 401(k) into an IRA, you can’t make a rollover from the IRA into yet another account until a year elapses.

- Your 401(k) rollover doesn’t count toward traditional IRA contribution limits. However, it will count toward your modified adjusted gross income, which can reduce your Roth IRA contribution limit.

- You can roll over a portion of your 401(k) and take the remainder as a payout. However, your payout is subject to income taxes. Plus, if you’re younger than 59.5, you’ll pay a 10% early withdrawal penalty. This age limit is reduced to 55 if you’re retired.

- You typically can retain your 401(k) even if you leave your old job. This option might be best if your new job doesn’t offer a retirement plan.

- If your 401(k) has less than $5,000 and you leave your job, you must instruct your plan administrator to keep your plan going. Otherwise, they might liquidate your account or roll it into an IRA without your approval.

- If your 401(k) has less than $1,000, your administrator will liquidate your account and send you a check.

- Keeping company stock in the original 401(k) is best. If you roll it over, you’ll be liable for net unrealized appreciation Holding the stock in the same 401(k) will help you receive optimal value from the stock when you decide to liquidate it.

Risks of Rolling Your 401(k) Into an Annuity

Annuities can be profitable options for your rollover, but they have specific drawbacks:

- Annuities can have high fees, especially if you add multiple riders.

- Annuities have what’s called an annuitization phase during which withdrawals are penalized. So, you usually must wait at least seven years before moving money out of the account. Otherwise, you’ll pay surrender charges.

- An annuity generally won’t pay a death benefit to your beneficiary if you don’t have a specific rider. Generally, the insurance company absorbs the money in your account upon your death.

- Annuities usually have lower growth rates than other investment accounts. Therefore, an annuity will likely take longer to reach a $1 million balance than a stock portfolio.

Rollover Tax Consequences

401k rollover to annuity

The average 401(k) rollover doesn’t have tax consequences. For example, when you conduct a direct rollover after starting a new job, you don’t touch the funds at any point. Instead, plan administrators handle the transfer, and the IRS isn’t involved.

On the other hand, you have 60 days with indirect rollover before tax implications occur. Specifically, if you don’t finish the rollover within this time limit, the government considers the money received as a withdrawal and will charge income taxes accordingly. In addition, you’ll pay early withdrawal penalties if you’re under age 59.5 and still working or under 55 and retired.

Because indirect rollovers don’t always go as planned, the IRS withholds 20% of all 401(k) payouts. This way, it can extract the tax payment due if you fail to finish a rollover before 60 days is up.

This rule can put you on a tight timeline if you’re shopping for an annuity. Therefore, it’s best to select your annuity before initiating a rollover. Then, you can tell your 401(k) manager to send the check directly to the annuity company. Doing so prevents you from acting as the middleman and gets the money where it needs to go.

Remember, matching contributions on a Roth 401(k) has unique tax consequences when rolling over. Although a Roth 401(k) uses post-tax dollars, your employer’s contributions are pre-tax held in a traditional 401(k). Therefore, your rollover must account for both Roth and traditional 401(k) funds.

Fortunately, you can roll the funds into new Roth and traditional accounts if your new employer offers both types. Likewise, if you’re converting to IRAs, you can use Roth and traditional accounts as needed. However, placing the matching funds into a Roth account will incur income taxes.

Best Practices for Rolling Over a 401(k) Into An Annuity

If you’re considering rolling your 401(k) into an annuity, follow these best practices to optimize your finances:

Understand Annuity Types

Annuities come in fixed, fixed indexed, and variable varieties. Fixed annuities earn a low interest rate, can guarantee payments for life, and won’t suffer capital losses. On the other hand, fixed indexed and variable annuities have higher earnings because they tie gains to stocks and other assets.

However, these annuities might cap gains when the stock market does well or lose value when it dips. Therefore, they are more volatile and usually aren’t eligible for 401(k) rollovers. So, going with fixed is the most reliable option.

Postpone Payments to Increase Income

Like Social Security, your annuity payments usually increase if you delay taking them. For instance, buying a $1 million annuity at 55 and waiting five years will create an annual income of about $90,000. However, buying the same annuity and waiting 20 years for your first payment will increase your annual income to over $200,000.

Don’t Overfund the Annuity

Annuities have specific funding thresholds before providing distributions. For example, your annuity might require $500,000 before you can withdraw payments. That said, $1 over this target doesn’t serve a purpose. So, let’s say you leave your job at age 50 with $250,000 in your 401(k). You’ve also been contributing to a $500,000 annuity throughout your career. Your annuity account has $450,000, meaning you need $50,000 more to fund it fully.

In this case, you can roll over $50,000 from your 401(k) and keep the rest in the account. This option will fulfill your annuity conditions and leave you with a sizable chunk of money to continue investing in stocks, bonds, and more.

The Bottom Line

Rolling over a 401(k) is usually a straightforward process in which your plan manager and new employer handle the cash involved. If you have your new plan information ready, you can have your money sent to your new plan without suffering any tax implications. However, if you receive the money, you have 60 days to get it into a new investment account without incurring tax consequences.

In addition, annuities are excellent options for rolling over if you aren’t getting another 401(k). Annuities offer guaranteed payments throughout the rest of your life. However, they can have high fees and no death benefits, so shopping around for the best deal is a good idea. Overall, it’s best to have a thorough plan before initiating a rollover to avoid consequences and retain your entire nest egg.

Tips for Rolling a 401(k) Into an Annuity

- A financial advisor can help you make the best rollover choices. Finding a financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to three vetted financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. If you’re ready to find an advisor who can help you achieve your financial goals, get started now.

- You can delay Social Security payments just like annuity distributions. Doing so can strengthen your financial position in retirement. Here’s why delaying Social Security is more lucrative than ever.